Batteries caught up in US-China uncertainty

Geopolitical tests for Ford and CATL, Tesla and China, lithium and sodium

Thanks for reading Here It Comes, my newsletter on the interactions between US-China relations, technology in China, and climate change. All-access subscriptions are free. Readers who especially wish to support this effort, and have the means, can contribute directly through a paid subscription. –Graham Webster

Here It Comes is back after a quiet period as I got ready for vacation and spring teaching, went on a fantastic vacation, and then started teaching. Since last issue, I’ve been collecting reading on battery markets in the US-China context, and there’s been a lot of action.

This edition covers three developments that on the face of it seem separate, but in the end look connected: Ford Motor’s adventure setting up a battery plant licensing Chinese technology for manufacture in the United States, Tesla’s announcement of a new factory for large-scale batteries in Shanghai, and China’s leading development of sodium-based battery tech while the lithium-based market fluctuates.

By the way, shameless plug: The Stanford DigiChina Project, which I lead, is now publishing most new articles individually on its newsletter. Check it out:

Now on to the batteries…Chinese battery leader CATL faces friction in US deal with Ford—and from Chinese regulators

The announcement in February that Ford Motor Co. would license technology from the global EV battery leader CATL to produce batteries in a Ford-owned plant in Michigan sure looks like a victory for several actors. Fujian-based CATL gets revenue out of exposure to the US market—probably a lot less than it would get simply manufacturing batteries and selling them to Ford, but more than the pittance that is a real possibility going forward given incentives for US consumers to buy US-made batteries. Ford gets to sell a bunch of America-sized Mustang EVs with advanced battery technology. China and the United States get a model of how business might still be done despite ever-rising bilateral friction—an elusive “win-win.” And the United States spins up more domestic production of EV batteries and more manufacturing jobs, in line with the Inflation Reduction Act (IRA)’s goals.

“The manufacturer considered sites in Canada and Mexico,” FT reported, “but chose to set up the plant in southwestern Michigan because of provisions in the IRA that encourage US manufacturing.” Indeed, much as Chinese policy for decades has traded market access for joint ventures, technology transfer, or other concessions by foreign firms, the United States has gone and done some industrial policy.

Unsurprisingly, some don’t see the deal as a win-win-win-win. Senator Marco Rubio (R-FL) called CATL founder Robin Zeng a “high-ranking member of the Chinese Communist Party’s ‘United Front’” and introduced legislation to “significantly restrict the eligibility of IRA tax credits and prevent Chinese companies from benefitting.” (Of course, Rubio opposed the IRA in the first place and seems to think the United States can just adapt to climate change and shouldn’t bother trying to minimize it.) Republican Virginia Governor Glenn Youngkin didn’t want the Ford jobs in his state, calling the plant a “trojan horse.” Even in China, there is skepticism, with regulators reportedly nervous that US policy could produce a tech-for-market-access situation out of their own playbook—a concern Senator Mark Warner (D-VA) rightly noted was “ironic.”

Yet CATL’s troubles aren’t just tied up with its US travails. The China Securities Regulatory Commission recently “issued window guidance—the industry term for informal instructions—for CATL to downsize to $1bn or less its plan to raise $5bn via a Swiss secondary listing,” FT reported, with the paper’s sources speculating about whether China’s government views the company’s enormous size as a problem.

More on CATL:

At CFR, Seaton Huang has a good summary of the Ford-CATL news.

Henry Sanderson’s book Volt Rush is excellent (so far, in the case of this reader), and The Wire China published an excerpt on CATL.

Eliot Chen wrote about Virginia’s decision to reject the Ford-CATL plant for The Wire China.

Tesla announces grid-storage battery plant in Shanghai

Tesla on April 9 announced plans for a new large-capacity battery factory in Shanghai, posting a photo from a signing ceremony between the Lin-Gang Special Area of the Shanghai Free Trade Zone and Tesla’s Shanghai subsidiary, which already produces cars there. The company apparently registered a new firm, Tesla (Shanghai) New Energy Co Ltd, to run the so-called “Megafactory” producing “Megapacks” and reportedly said it would start construction in the third quarter of this year and begin production around this time next year.

The announcement was condemned by some, including Jacob Helberg, a member of the U.S.-China Economic and Security Review Commission (and a fellow affiliate of the Stanford Cyber Policy Center), who called for the investment to be blocked and for rapid implementation of US outbound investment limits reportedly under consideration by the Biden administration.

Tesla already produces its “Megapack” batteries, for applications including storing energy to balance peak renewable generation and peak demand on electric grids, in Lathrop, CA. The company advertises the production capacity of the existing California plant and the announced Shanghai plant as an identical 10,000 units per year.

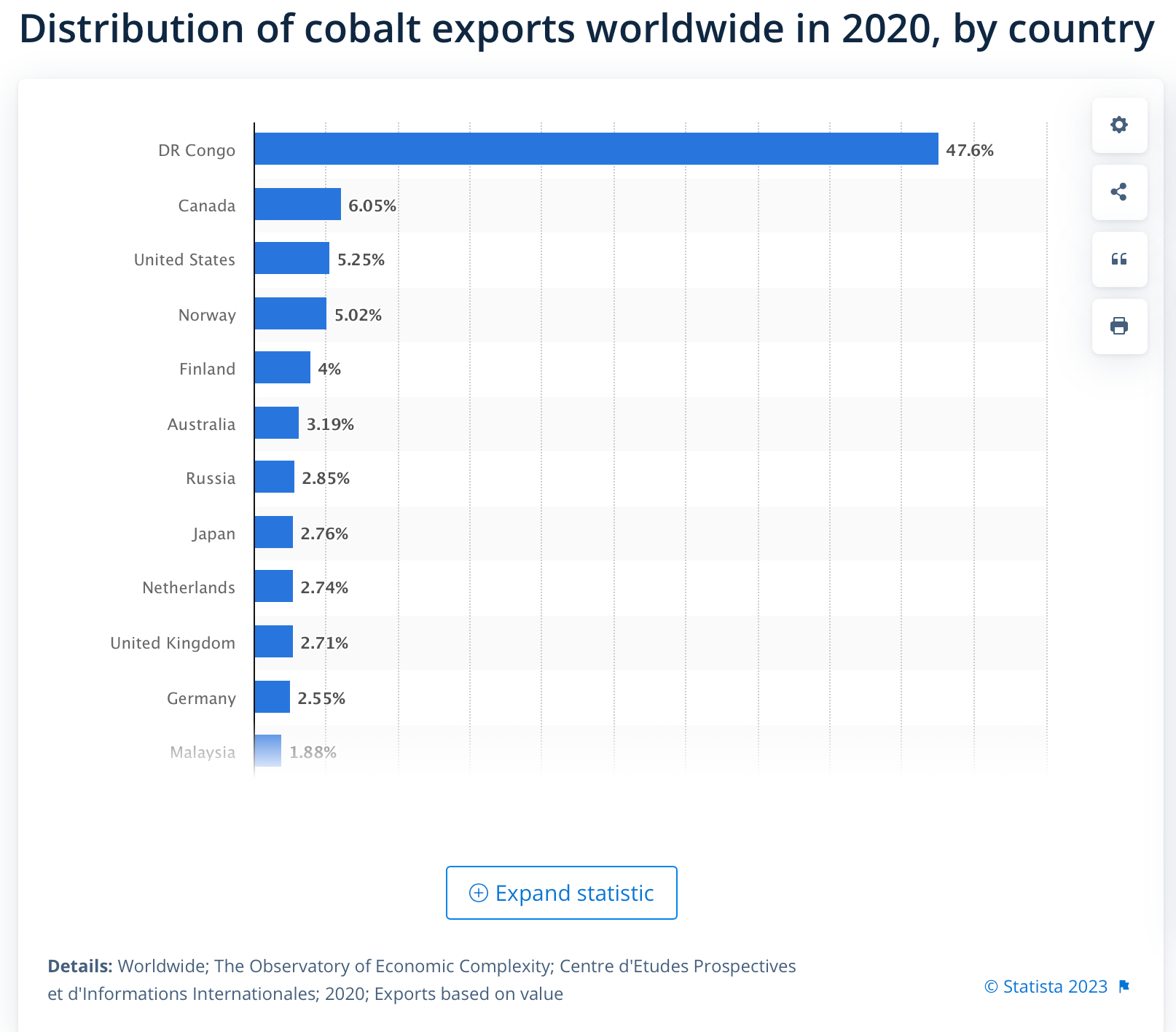

Numerous industry publications have reported that Tesla as of recently planned to switch its megapacks to lithium iron phosphate (LFP) chemistry, which the US National Renewable Energy Laboratory describes as the “primary chemistry for stationary storage starting in 2021.” LFP contrasts with the previously more common lithium nickel manganese cobalt oxide (NMC) in terms of both application and human impact. Unlike NMC, LFP does not rely on cobalt, nearly half of which in 2020 was mined in the Democratic Republic of Congo.1 There, worker conditions are “on par with old-world slavery,” according to Siddharth Kara, a Harvard fellow and author of the book Cobalt Red.

Oh, and that LFP chemistry? That’s the technology CATL can contribute to Ford’s battery plant in Michigan, freeing that new production capacity from entanglement with the cobalt trade.

Meanwhile:

Tesla is rumored to be looking at building a US battery plant using CATL’s LFP tech.

China poised to lead transition from lithium- to sodium-based battery tech, NYT reports, as China’s battery industry fluctuates

I wasn’t lingering there on the chemistry question just to sound smart. Keith Bradsher of The New York Times made some sparks in this battery-charged news cycle2 with a story on Central South University and the broader industrial ecosystem around Changsha, Hunan, where sodium-based battery chemistry is being developed toward market.

Bradsher writes that sodium’s advantages over lithium (which is at the center of both NMC and LFP batteries) include being hugely common, cheap, and cold-tolerant in battery chemistry. Its disadvantages include requiring larger cells for the same power storage, making sodium chemistry more immediately competitive for grid storage than for electric vehicles or other portable applications. Like the LFP chemistry, sodium tech does not rely on cobalt.

The article got the attention among the geopolitical classes most likely because of its headline frame—“Why China Could Dominate the Next Big Advance in Batteries”—and because of story arcs like this:

Research into using sodium for batteries began in earnest in the 1970s, led then by the United States. Japanese researchers made crucial advances a dozen years ago. Chinese companies have since taken the lead in commercializing the technology.

Out of 20 sodium battery factories now planned or already under construction around the world, 16 are in China, according to Benchmark Minerals, a consulting firm. In two years, China will have nearly 95 percent of the world’s capacity to make sodium batteries.

The lithium battery industry in China more broadly looks like it’s on a roller coaster this year, with prices for the industrial input lithium carbonate falling rapidly after a massive increase from late 2021 to a peak in November 2022, according to a feature in Caixin. The lithium price bulge reportedly mirrored a period when demand exceeded production, followed by a period of supply outpacing demand.

The Caixin article on the Chinese battery industry’s travails, published April 7, noted layoffs at CALB, the country’s third-largest producer, and reported an industry analyst suspected only CATL and BYD (the two largest) operated at over half of their capacity in January and February.

The conclusion of the Caixin story ties pretty much all of this edition together:

CATL and Ford Motor Co. in February announced a battery plant in Michigan with a novel ownership structure under which Ford would own 100% of the plant, including the building and the infrastructure. CATL is to “license its intellectual property for battery technologies to Ford.” Some analysts were concerned about the model of “technology in exchange for orders.”

Europe is likely to be an easier option for Chinese battery companies. CATL, SVOLT Technology, EVE Energy and Gotion have unveiled plans to build five factories in Germany with a total planned capacity of 74 GWh. In Hungary, CATL said it plans to invest about 7.3 billion euros ($7.9 billion) to build a 100 GWh production line.

Europe will be the most important region for Chinese battery companies going global as many large European automakers are seeking suppliers, Teng Yong, a global partner at consulting firm A.T. Kearney, told Caixin.

As geopolitical tensions intensify, Chinese battery companies are slowing the pace of going abroad. Some of the projects were just announced but haven’t started construction, said a person who’s in charge of a Chinese battery company’s overseas business.

Compared with building factories overseas, the risk of entering the energy storage business is relatively small, with a clearer industry policy outlook. China’s top 10 domestic power battery suppliers have all laid out plans to tap into the energy storage business.

So there you have it. People need batteries all over the world. China has some of the most intensive domestic competition and some of the most competitive firms globally in batteries. Building batteries with Chinese tech in the United States is making US politicians nervous, which is making Chinese battery firms nervous about going big abroad. Meanwhile, Tesla is expanding its large-capacity storage battery manufacturing to China and considering building batteries with Chinese tech in the United States, and Chinese battery firms are looking to large-capacity storage projects as a safer bet for getting business abroad. At least that’s part of the picture.

Comments? Criticisms? Reading recommendations? Drop me a line.

About Here It Comes

Here it Comes is written by me, Graham Webster, a research scholar and editor-in-chief of the DigiChina Project at the Stanford Cyber Policy Center. It is the successor to my earlier newsletter efforts U.S.–China Week and Transpacifica. Here It Comes is an exploration of the onslaught of interactions between US-China relations, technology in China, and climate change. The opinions expressed here are my own, and I reserve the right to change my mind.

Data from the Observatory of Economy Complexity via Statista.

I allowed myself exactly one (1) terrible battery quip today.